- Joined

- May 9, 2013

- Messages

- 4

- Reaction score

- 0

Just a few questions and thoughts I had about Public Service Loan Forgiveness...

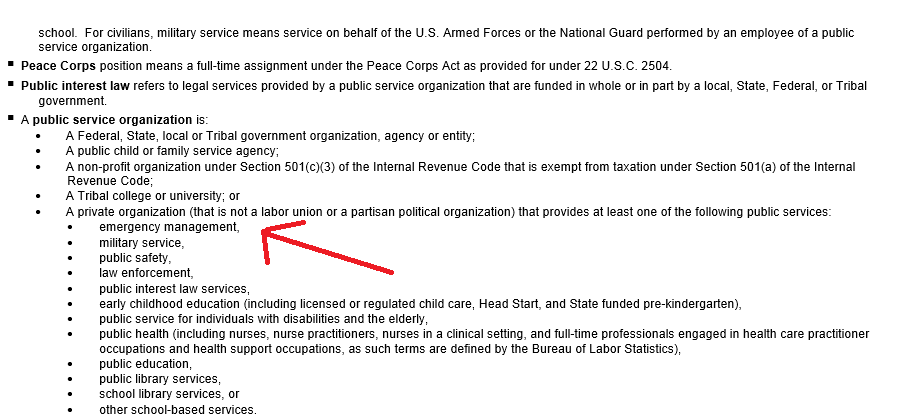

For the Public Service Loan Forgiveness, does working at any hospital that has an Emergency Room count? Even if it's nonprofit? Based on how I'm reading the ECF form for it, it would seem to indicate so! Thoughts?

Source: https://studentaid.ed.gov/sites/default/files/public-service-employment-certification-form.pdf

Secondly, has anyone thought about how states with laws preventing hospitals from hiring physicians directly would effect trying to do PSLF in that state? If you can't work for the eligible nonprofit due to such rules, how would this play out? Who would actually be the employer that would qualify in such a case? I'm a little lost on this one, any help?

(States with such laws include California and Texas http://www.amednews.com/article/20090803/profession/308039984/2/)

Finally, has anyone found a good online calculator that shows monthly payment amounts through residency and the jump in income after residency for Income Based and Pay as You Earn plans?

For the Public Service Loan Forgiveness, does working at any hospital that has an Emergency Room count? Even if it's nonprofit? Based on how I'm reading the ECF form for it, it would seem to indicate so! Thoughts?

Source: https://studentaid.ed.gov/sites/default/files/public-service-employment-certification-form.pdf

Secondly, has anyone thought about how states with laws preventing hospitals from hiring physicians directly would effect trying to do PSLF in that state? If you can't work for the eligible nonprofit due to such rules, how would this play out? Who would actually be the employer that would qualify in such a case? I'm a little lost on this one, any help?

(States with such laws include California and Texas http://www.amednews.com/article/20090803/profession/308039984/2/)

Finally, has anyone found a good online calculator that shows monthly payment amounts through residency and the jump in income after residency for Income Based and Pay as You Earn plans?