- Joined

- Jan 14, 2004

- Messages

- 962

- Reaction score

- 126

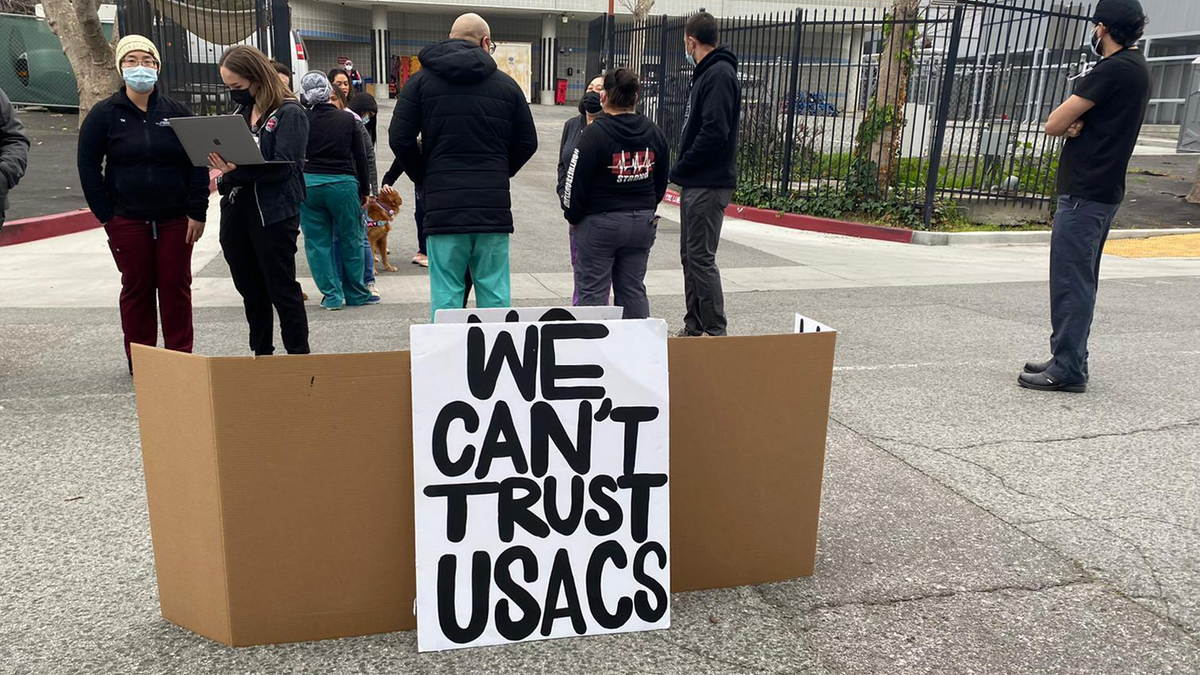

Out Of The ER, Into The Street

Enraged by Wall Street’s takeover of their profession, emergency physicians are rising up and speaking out.

www.levernews.com

www.levernews.com

www.levernews.com

www.levernews.com

Absolutely terrifying honestly. Didn't know that was even looming on the table.If Apollo really buys Envision, that’s the endgame no?

Wait what? Isnt Apollo a tiny group compared to Envision? Wouldn’t the opposite scenario be more likely?If Apollo really buys Envision, that’s the endgame no?

I believe that Apollo MD is different than the Apollo private equity behemoth.Wait what? Isnt Apollo a tiny group compared to Envision? Wouldn’t the opposite scenario be more likely?

Yeah, Apollo MD has nothing to do with Apollo global management. I believe they have a different PE partner.I believe that Apollo MD is different than the Apollo private equity behemoth.

If Apollo really buys Envision, that’s the endgame no?

While doctors may technically own USACS, the majority of its profits are controlled by the half-trillion dollar private equity firm Apollo Global Management. According to the USACS statement provided to The Lever, “Apollo is a supportive lender to USACS and in 2021 provided financing to enable our physician-led buyout, giving doctors full control of our business when our former capital partner sold their minority equity stake… Apollo is a supportive lender, but has no right to exert operational control at USACS.”

But that financing means that barring some miracle, Apollo likely controls the company’s destiny — since that capital came with what appear to be virtually impossible terms.

In several deals it called “a form of hybrid capital,” Apollo agreed to buy a total of $711 million in preferred USACS stock that would convert into something akin to high-yield debt in five years if management couldn’t come up with the funds to buy it back.

A USACS employee and shareholder told The Lever they have been repeatedly told by corporate representatives that the “interest rate” on Apollo’s investment is 10.5 percent. That means that every year, USACS needs to pay its investors at least $75 million in dividends, which is roughly half of what the Moody’s credit agency estimates the company earns every year. Those payments would likely be a lot easier to manage if USACS didn’t have an additional $725 million in old-fashioned debt, taking another $47 million or so in annual interest expenses out of its coffers.

It’s possible that USACS will pull off an earnings surprise: Its numbers were good enough in 2021 that USACS spent $132 million on dividends, transactions, and share buybacks in the third quarter, according to Moody’s. But Moody’s, for one, described the terms of the Apollo deal as a veritable guarantee that USACS’ financial structure will experience a “material change” within the next five years — which is bond-lawyer-speak for, “physician owners are going to get wiped out.”

If Apollo really buys Envision, that’s the endgame no?

ApolloMD is not owned by a private equity and we have nothing to do with Apollo Global Management.

ApolloMD is physician owned.

Envision has been not-so-secretly planning to split itself into two. Various news-sources have reported on the fact that, even if Envision won't formally confirm it: anonymous 'leaks' match corporate restructuring moves that are publicly visible. Plan appears to be to split the company in two between profitable and unprofitable hospitals and sell the unprofitable ones off to whomever will pay the highest for those bad assets. Because these private equity groups make their money if the company succeeds but also make money if the company fails - as shown in USACS. They bail the company out for massive amounts of money with the deal that later on the piper will get paid and if it has to sell off the hospitals or bankrupt the whole company to do so - it will let that happen.

But this group apollo wont buy all of envision only part, but envision will likely shrink by 40-ish percent one day and suddenly someone else will be holding the bag on that 40% that 'left' the company.

The conversion to debt ensures they gets paid. To oversimplify it:I think I understand the "heads Envision wins" part re keeping the profitable contracts. I'm struggling with the "tails PE wins".

If I understand correctly, the start of the "tails PE wins" part would be Envision selling, eg, their unprofitable BFE Medical Center ("BFE") contract to PE, eg Apollo or Blackrock, which PE buys with money that PE borrowed from, uh, somewhere... ultimately taxpayers' future earnings basically?

PE then writes BFE a long, arcane contract in which BFE grants PE "equity", which at the time looks to BFE like basically a part of BFE's future earnings, if any. This makes PE look like heroes to the outside world who will "turn around a failing ER" because there is ¡no debt no chains YAY CAPITALISM!

Except... in that arcane contract that no one actually bothered to read because they were too busy eating the delicious sammiches that PE bought them at the presigning party, PE actually inserted a poison pill that says this equity is actually just like debt, in that if a random huge amount of money x that PE chose is not paid to PE by BFE within n years, the x amount of equity gets converted to x amount of debt.

And then of course BFE can't pay the equity within n years, because they aren't profitable and never will be because it's BFE, and now BFE is in chains to PE.

Am I understanding this right?

If so, what happens next? Where would the money ultimately come from to pay PE, if the deal didn't include dumping the "equity" on the gullible docs (like USACS) and the BFE contract includes no real assets (like any ER contract)? Who is the greatest fool?

Would PE depend in that case on the Fed put, if that's still a thing? Ie, someone needs to staff the ER at BFE, or else sick BFers have no ER and inappropriately suffer and die, so the government ultimately buys the contract from PE? Thus completing the circle of PE looting from taxpayers?

Bolded is the part I fail to understand.B: Failure. Stock is converted into preferential debt as a secured creditor. Envision either cobbles together the money to pay PE (PE wins) or Envision files for bankruptcy and is forced to liquidate assets in order to pay creditors. As a secured creditor, PE is the first to get paid. PE wins. The only scenario where PE loses here is if Envision is so grossly mismanaged that they not only fail to become profitable, but they drive all of their remaining asset values so far into the ground that they exceed the debt that is owed to PE (unlikely).

What kind of "assets" does a staffing company have to sell off?The only scenario where PE loses here is if Envision is so grossly mismanaged that they not only fail to become profitable, but they drive all of their remaining asset values so far into the ground that they exceed the debt that is owed to PE (unlikely).

No, we aren't owned by ValorBridge. There is a relationship with them, but they do not own ApolloMD. Chris Durham was with ApolloMD when he founded ValorBridge. They still maintain investments in ApolloMD, but ApolloMD remains a majority physician-owned company (not sham stocks like some CMGs have done).ValorBridge Partners?

So we're talking about slightly different things here. I was referring to KKR's general strategy with Envision as a whole. Not necessarily with this spin off, though if Envision does split into 2, I suspect that KKR will probably use the opportunity to eject from both Envision and the spin-off company seeing as they're right on schedule for the usual 5 yr PE healthcare cycle.Bolded is the part I fail to understand.

I thought the whole point is that Envision doesn't own the unprofitable parts anymore because they sold them to PE. Envision kept their profitable parts and won ("heads").

Suppose we call the unprofitable parts "Enblinden" and they fail to cobble together the money to pay PE. So "Enblinden files for bankruptcy and is forced to liquidate assets in order to pay creditors."

I thought the whole point is that Enblinden only owns BFEs, ie pieces of paper that give them a right to the future earnings of BFE's ER. But by definition there are no future earnings, ie all the BFEs are unprofitable; otherwise Envision wouldn't have spun them off.

So, what assets does Enblinden actually have with which to pay creditors? Ie, how does PE expect to make any money at all in this case, which I consider the most likely, unless Enblinden goes full USACS and fleeces new docs to pay PE?

Thanks for the clarification that "poison pill" is a technical term. Is there another preferred phrase in Financeland to describe this occult equity->debt conversion maneuver? "Lying by omission" is the first alternate phrase that comes to my unwashed mind.

ApolloMD is as physician owned as apple and target.ApolloMD is not owned by a private equity and we have nothing to do with Apollo Global Management.

ApolloMD is physician owned.

I think I understand the "heads Envision wins" part re keeping the profitable contracts. I'm struggling with the "tails PE wins".

If I understand correctly, the start of the "tails PE wins" part would be Envision selling, eg, their unprofitable BFE Medical Center ("BFE") contract to PE, eg Apollo or Blackrock, which PE buys with money that PE borrowed from, uh, somewhere... ultimately taxpayers' future earnings basically?

PE then writes BFE a long, arcane contract in which BFE grants PE "equity", which at the time looks to BFE like basically a part of BFE's future earnings, if any. This makes PE look like heroes to the outside world who will "turn around a failing ER" because there is ¡no debt no chains YAY CAPITALISM!

Except... in that arcane contract that no one actually bothered to read because they were too busy eating the delicious sammiches that PE bought them at the presigning party, PE actually inserted apoison pillsuper-secret weaselly clause that says this equity is actually just like debt, in that if a random huge amount of money x that PE chose is not paid to PE by BFE within n years, the x amount of equity gets converted to x amount of debt.

And then of course BFE can't pay the equity within n years, because they aren't profitable and never will be because it's BFE, and now BFE is in chains to PE.

Am I understanding this right?

If so, what happens next? Where would the money ultimately come from to pay PE, if the deal didn't include dumping the "equity" on the gullible docs (like USACS) and the BFE contract includes no real assets (like any ER contract)? Who is the greatest fool?

Would PE depend in that case on the Fed put, if that's still a thing? Ie, someone needs to staff the ER at BFE, or else sick BFers have no ER and inappropriately suffer and die, so the government ultimately buys the contract from PE? Thus completing the circle of PE looting from taxpayers?

What kind of "assets" does a staffing company have to sell off?

I suspect someone from inside USACS who got his/her pockets nicely lined by the PE group to sign off on the deal.So USACS has a potential debt of 1.4b in 5 years at 10% interest with an annual revenue of 150M. So who signed off on this deal?

I'm not arguing in a forum for somebody who has no direct knowledge of ApolloMD operations.ApolloMD is as physician owned as apple and target.

Team

OUR TEAM Christopher Durham Chris successfully co-founded ApolloMD with Gerald Bortolazzo, MD to support the clinical operations of a rapidly growing clinician group. He continues to serve in a...www.valorbridge.com

Ah, this was the huge important thing that I was missing. So, "BFE" really does mean part of BFE and not just the paper BFE ER contract, and PE will have its claws in some real hospital assets to sell if they are unlucky and happen to be holding the hot potato before their C-suite turns over again.Envision (enblinden?) made this entire system extra efficient by partnering with the hospitals in a way that makes them part owners of the hospital (only part). It allows them to have some access to hospital assets in the situation where they tank. I should have clarified.

Their revenue before vep and Alteon was just under $1b. I think about $1,5b now.I suspect someone from inside USACS who got his/her pockets nicely lined by the PE group to sign off on the deal.

No problem lol.I'm not arguing in a forum for somebody who has no direct knowledge of ApolloMD operations.

That's a lot of revenue.Their revenue before vep and Alteon was just under $1b. I think about $1,5b now.

Those numbers vastly different from the ones implied in the article above. Unless I missed something.....Their revenue before vep and Alteon was just under $1b. I think about $1,5b now.

I trust moodys. “its pro forma revenues (including Alteon acquisition) are approximately $1.5 billion.”Those numbers vastly different from the ones implied in the article above. Unless I missed something.....

Why did no one want their stock? Does PE see this $100--150M profit as particularly low relative to other CMGs?Issue is their profit is in the $100-150m range.

Interest will be $80m.

If you read the article you will see they have to pay the debt off by 2026 or Apollo basically controls the company.

In reality I would expect them to refinance their debt. There is no chance they can pay it back. They can only refinance it.

It wasn’t usacs preference to take on debt. Wcas wanted out and no one wanted their stock. Preferred stock (favorable debt) which will allow them control and diminishes their risk. It’s basically the crappiest terms you can get as a company. Like borrowing from a loan shark.

Worked for VEP for years, USACS just cut our pay by 18% (in addition to cut in benefits from when the "merger" happened).I think they can and will cut costs. I have spoken to app and this is their plan. Drive pay down asap. It was then in their offering slide deck.

You were in the VEP merger cohort too, huh?Worked for VEP for years, USACS just cut our pay by 18% (in addition to cut in benefits from when the "merger" happened).

In retrospect, I wish I had never learned about VEP either. USACS, I knew, because they had already invaded my hometown and driven down pay by $25/h around the time I finished residency. (And subsequently bailed and were replaced by Envision at the same lower pay rates.)Guess, I’ve been out of the loop. Didn’t realize that VEP and USUCK merged.

I'm a PA. VEP gave us an average pay with a decent bonus available for RVU bonuses. USACS kept us at our historical pay+RVU level for a while but just changed it. Under USACS it seems near impossible to get any bonus.Did you choose the W-2 $20/h straight-up pay cut or the 1099 pay-our-taxes-now-serf 83(b) option?

I'm a PA. VEP gave us $70/hr with an RVU bonus that a few of us could get up to $85/hr. USUKS kept us at our historical level ($85) for a few months as billing shifted over but then suddenly I can't make much more than $70/hr anymore.

Nope, too old for that.For some reason I thought you had gone to med school after the PA.

I guess you were as surprised by this merger as I was. I joined about 6 months before, and I figured VEP was there to stay and there were no unknown unknowns. But, I guess the thing about unknown unknowns is you can't really know about them. You know?

I'm sorry to hear about your big pay cut. It's an awful situation, and I guess it's all relative. USACS just straight-up laid off our PAs without much warning after the merger. Has caused a bit of drama at my shop.

Yes, this was my conclusion as well. I was lucky to have a connection at a W-2 hospital-employed gig that seems more sustainable.At the risk of beating the same drum over and over...anybody looking for a job needs to find a hospital-employed/VA/Kaiser/DoD/IHS gig. Sure, a genuine unicorn sdg that doesn't have a predatory pre-partner track is the most ideal -- if you can find it.

And if you're not currently looking for another gig but still work for a CMG, you need to be looking at one of the above places. Even if it's just prn to start. Get your foot in the door however you can.

That would require getting around the non compete clauses…No appetite here to take back contracts? I mean USACS only owns contracts no actual product. We the docs are the product. Why not take over their contracts. Seems no appetite to even try. I think would be wise to gather a small group together and work with embc or aaempg and get some help when things implode for envision app USACS etc.

Crazy. My thoughts exactly. Anyone else have advice on working for the VA? Looks like the best bet around hereAt the risk of beating the same drum over and over...anybody looking for a job needs to find a hospital-employed/VA/Kaiser/DoD/IHS gig. Sure, a genuine unicorn sdg that doesn't have a predatory pre-partner track is the most ideal -- if you can find it.

And if you're not currently looking for another gig but still work for a CMG, you need to be looking at one of the above places. Even if it's just prn to start. Get your foot in the door however you can.

I think it's an awesome idea in theory. Fight the power!No appetite here to take back contracts? I mean USACS only owns contracts no actual product. We the docs are the product. Why not take over their contracts. Seems no appetite to even try. I think would be wise to gather a small group together and work with embc or aaempg and get some help when things implode for envision app USACS etc.

I'm moving on to better, much higher paying job. Will stay part time at this shop because it is a great team there. I would do damn near anything for the docs I work with.

Can have your friend who doesn’t work there get the contract and then u can work there and then get ownership once that’s gone. Will be curious if the ftc removes that.That would require getting around the non compete clauses…