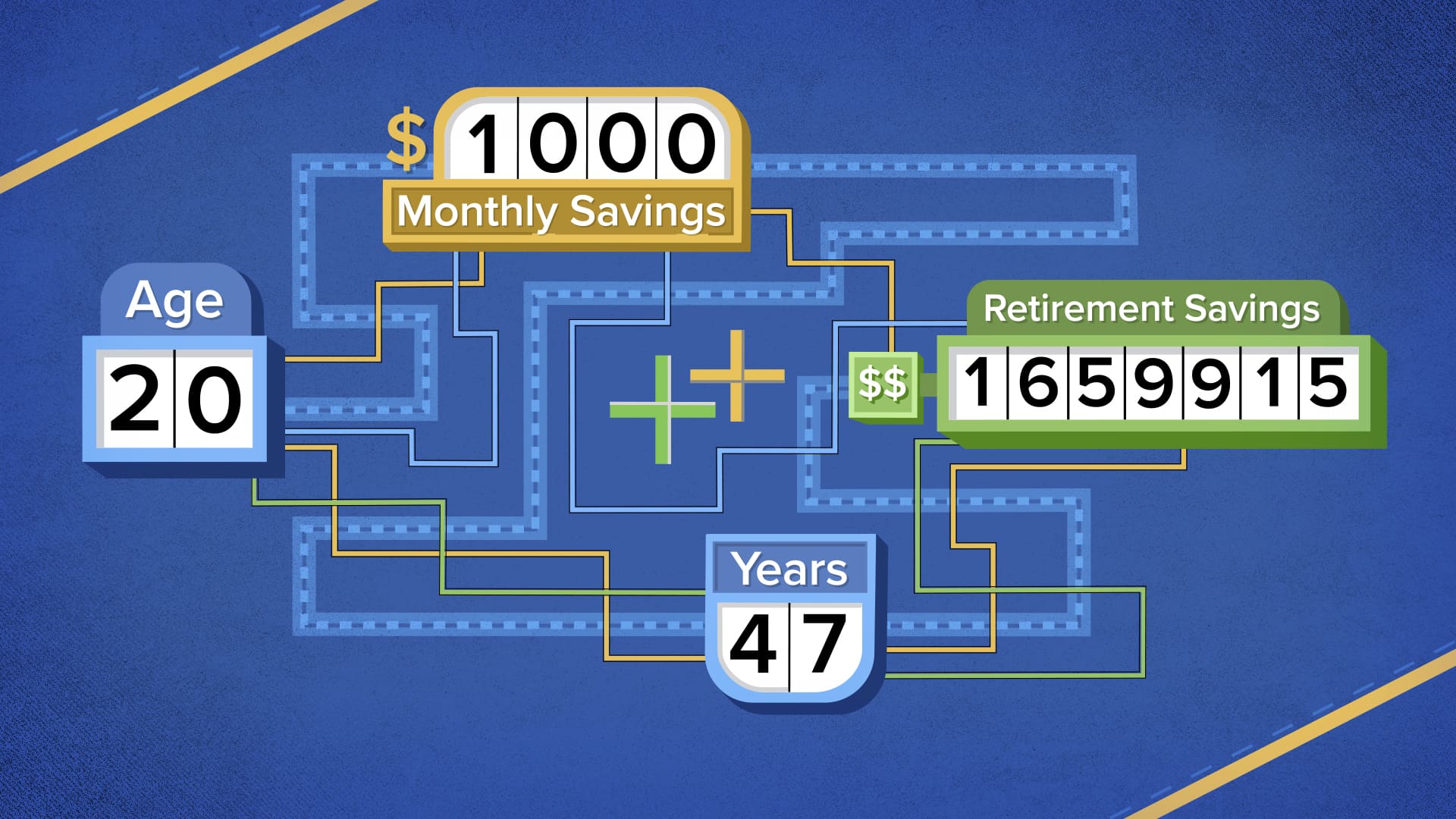

Let's get back on track here. Hypothetically, Southpaw wants to retire at age 50. What is a good estimate for his nest egg number if he wants to stop working entirely? Traditionally, the number of 25 X required income was the answer. So, if Southpaw wants $200K in income he would need $200K x 25.

But, because Southpaw is retiring early and things are less certain the earlier you retire Southpaw needs 33 X $200K or $6.6 million. The reason is the initial withdrawal rate, IWR, of 4% could be too high to last his lifetime. Again, the earlier you retire the lower the IWR or the more money you need saved up.

The 25x Rule of retirement savings is a reasonable approach for those retiring at a traditional age.

For extreme early retirement, however, a 33x Rule may be more appropriate. Further, market valuations and a retiree’s specific asset allocation can have significant effects on a safe IWR.

The 25x Rule helps you estimate the total amount of money you need to save for retirement. Planning for retirement involves countless considerations, from deciding when to take Social Security to paying for healthcare and managing retirement accounts. This useful rule of thumb can give you a high-le

www.forbes.com

In markets with high P/E ratios the safe IWR is lower than for those who retired during markets with low P/E ratios. This brings us back to what is a safe IWR for early retirement? In this stock market I would argue 2.5% is the right IWR for someone retiring at age 50 vs a 3.0-3.5% IWR for someone retiring at age 65.

Thus, Southpaw actually needs even more than 33 X his required income to retire at age 50 if we use a IWR of 2.5%. The numbers show that Southpaw needs closer to $9 million US dollars to retire at age 50 if he wants $200K in annual income after taxes/healthcare.

Remember, Southpaw can fix this issue by going 0.5 FTE at age 50 rather than retiring completely; this lowers his nest egg requirement dramatically and hedges the risk that the market crashes during his early retirement years.

BOTTOM LINE: The earlier you retire before age 65 the bigger the nest egg and the lower the IWR to safe guard against worst case scenarios.