- Joined

- Sep 20, 2016

- Messages

- 1,802

- Reaction score

- 502

- Points

- 5,221

- Age

- 49

- Location

- Texas

- Attending Physician

I don’t see how one would need anywhere near that much unless they blow money at a really impressive rate, plan to continue to do so for decades, and/or want to leave a substantial estate to someone/something.

My requirements are far lower, I have extreme longevity on both sides, and I’m not exactly thrifty.

No ex wives is the key in this equation.

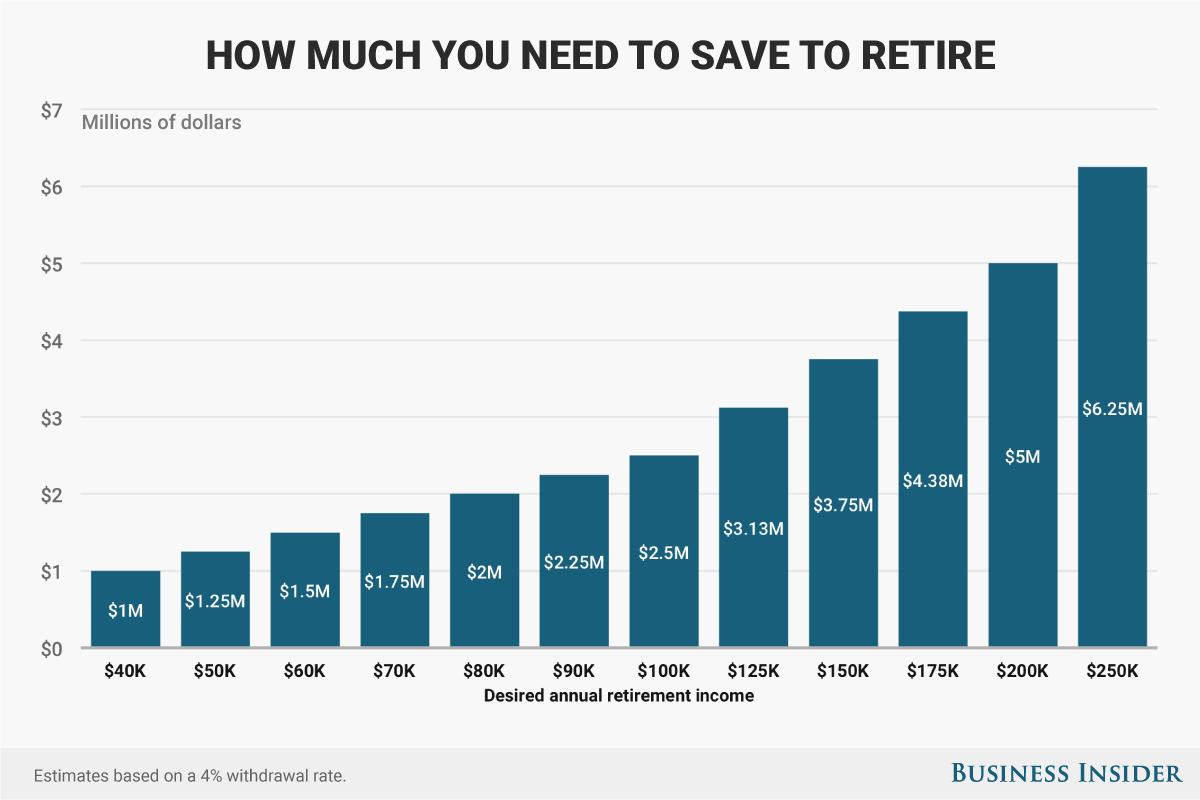

$5 million is about $150-200K/year of pre-tax spending money. That's not an outlandish lifestyle for a retired physician.

I don’t see how one would need anywhere near that much unless they blow money at a really impressive rate, plan to continue to do so for decades, and/or want to leave a substantial estate to someone/something.

My requirements are far lower, I have extreme longevity on both sides, and I’m not exactly thrifty.

No ex wives is the key in this equation.

--

Il Destriero

Particularly when you consider the effect of inflation and the market's propensity for volatility.

-If you aren't old and you ain't working, you are probably spending. I know I do.

-How much to budget for personal healthcare, including obtaining insurance?

-How long you plan to live?

-How much do you want to spend?

-How much you want to leave to heirs?

-How much risk that you want to take that financial markets won't do anything worse than they have in the last 100 years?

-How much of a cushion you want, just in case?

-How prudently you allocate your assets?

-Political risk of confiscatory, redistributionist tax policy? A lot can happen over a few decades.

-Natural disaster that wipes you out and being underinsured?

-Increased unanticipated need or desire to support loved ones?

There are plenty of black box financial calculators that will spew out lots of precise, but not necessarily accurate data.

Short version, what you are looking at is what is known as a "sustainable withdrawal rate" Assuming that you have a reasonably prudent portfolio and financial markets don't throw us anything worse than the great depression, political risks don't show up, you are bullet proof with a 2% withdrawal rate, very probably safe at 3%, probably OK at 4%. Allows for inflating contributions.

Anything more than that you are taking some risk of running out of money. Interestingly, assuming that the future is not that different from the past, there is not that much difference statistically in financial retirement risk of running out of money living 30 years vs living forever.

Roll the dice.

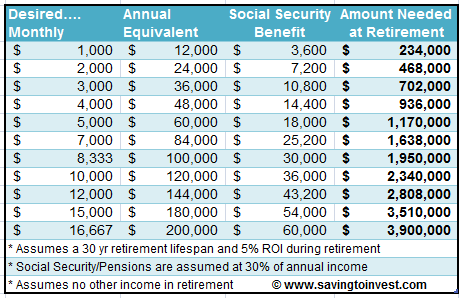

- 2% 10 million= $200K

- 3% 10 million= $300K

- 4% 10 million= $400K

I know. That's what I was getting at -- the 150-200K you cited are on the low end and should be pretty easily doable even with fluctuating market performance. I agree with both of you.A safe SWR incorporates both inflation and market volatility (the "sequence of returns" problem) in its claim of safety. Backtesting against history, picking the worst possible time to start retirement, even accounting for stock market crashes and periods of high inflation, it appears that - as dr doze noted in his post - 4% is safe, 3% is very safe, 2% is perfectly safe.

The reality is that those numbers are probably even safer than that, because those figures assume constant, robotic withdrawal, come hell or high water. People aren't robots. If the market dips or some other horrible event comes to pass, you're not required to spend exactly 4%. Maybe you travel less for a couple years and take 2%.

$10 million? That seems really high. I view retirement as a phase and not an event.

I have a fairly low number to cut call ($1.5-2 million)and another number to go part time. There are too many unknowns to put an exact number on it. We'll see how I feel when I get there. All I can do I maximize my savings and control my spending. Life is way too short to spend it sitting in an OR.

The problem with continuing to do anesthesia after accumulating higher levels of assets is the liability as well (especially with only a 1/3M malpractice insurance).

Forensic accountants will help malpractice lawyers target you for higher malpractice lawsuits over your insurance limits if they think you have considerable assets to target.

After a certain point, the NPV of the assets accumulated will be higher than the future revenues generated by continued anesthesia practice. Is it worth continued practice at that point considering the risk profile?

If the withdrawal was done through blue chip dividend stocks or even an SP500 Vanguard fund (1.85% dividend yield: Vanguard - Product overview - S&P 500 ETF), you could withdraw that money at a FAR lower tax rate than conventional income tax.

If had 10 million stashed in an SP500 fund, you could live off the dividends at 185,000/year that is taxed at a 15% rate. This yield would be equivalent to making about 300-350K per year income. Living off the dividends while allowing the principal to appreciate in the fund would be the ideal scenario.

That is where I got the idea of the 10M figure.

Even at 5M, that would produce about 100K/year in an SP500 fund with post tax of 85K/year (equivalent to 150-200K per year if earning an income) if you lived off the dividends whereby you let the principal appreciate.

Although not unheard of, actually losing personal assets due to malpractice is exceedingly rare. Assuming that you don't provide care while drunk or high or sexually assault your patients under anesthesia or do things that you absolutely have no business doing.

You could always buy lots of extra insurance. It's what I do and exceedingly simple. Fancy asset protection strategies are out there, but probably a waste of money. Especially if you live in Texas.

Dividend yield of the S&P 500 is not guaranteed, (like a Treasury Bond, chortle). That was the premise of the book "Dow 36,000" published in 1999. Essentially the author argued that dividends were rock solid as a treasury bond and that stock prices should be bid up to reflect this. How did that go?

BTW, tomorrow there is a treasury auction reopening of the 5 year TIPs. Anticipated real yield around 0.5%. Woo hoo. Throwing a chunk of IRA money at it. Not great, but better than a TIPs note has been in several years. Pretty good place to put your safe money.

Why does everyone at age 55-65 still plan on buying $100,000 cars and going on $20,000 vacations?

I’m not even 35 yet, but if I had $2-3M and owned a home outright, I’d drop everything and just be happy to never ever work again, and I’d do everything necessary to make that money last. In other words, I’d adjust my lifestyle so I can love comfortably.

I don’t know why people are so hung up on maintaining lifestyle. I make 4x as much as my parents did and they never struggled for mortgage, food, toys, vacations, or education. Homes in CA were a lot cheaper back then I guess.

In this job market and with the cost/time of getting a medical degree/career, it’d take me two lifetimes or a lucky bet on bitcoin many years ago to ever reach $10M.

My personal goal is similar to the OP's opening number but I may not get there. My withdrawal rate during retirement will be about 2-2.5% because I'm conservative. I could see a 3% withdrawal rate for others.

Another thing to consider is working part-time 2 days per week which would really reduce your overall "number" to retire earlier.

Seriously. Most people plan on retiring between ages 55-65 when they hit they magic number (in today’s money aka 2018). You ain’t gonna to live more than 20-25 years max. And u ain’t gonna to be a high roller after age 70.

How can you tell that? I am reading about 10-40 million dollar lawsuits almost weekly these days against physicians.

A buddy of mine just retired at 63 with $2mil, mortgage paid off, never divorced, and kids out of college. He is loving life and has plenty of money as long as he doesn't go crazy.Here's a life expectancy calculator from John Hancock.

55 year old male in good health can expect to live to about age 95. 65 year old male in good health can expect to live to about age 96.

Not going to live more than 20-25 years max???? Even allowing a median life expectancy in the US of like 75-80 years of age at this point, that includes everybody that dies young. Once you get to age 55 or 65 in good health, you can reasonably expect another 30+ years to go.

I work with colleagues who still go full time in their 70s and you'd probably still call them a high roller. You don't think if someone retired 15 years before that they couldn't maintain the same lifestyle as someone their age working full time? Damn. I'd be living even larger if I didn't have to bother with work.

For me, about $10M is my rough and tumble easy to think of number to walk away. I'd see it as basically $300K per year adjusted for inflation for life (because I'm always nervous and conservative and use 3% as my SWR guesstimate). Could I retire with significantly less? Sure. But why? I like my job and while I can be really frugal with some things, I have found very enjoyable ways to spend money that I'd like to continue to do without worry. And so to just up and walk away from a great paying career for good, I'd feel like I need near 100% certainty of maintaining my perfectly desired lifestyle forever.

Now that said, I'm not working forever to attain that $10M. To me that's the walk way early number. If I was 65 and had 5M I'd likely say I've had more than enough and don't want to work anymore. But still in my early to mid career, I'd need a lot to just walk away.

I believe max SS check is about 3 grand a month these days10Mil is huge: over a 30 year career that's 330k/annum even 5Mil is impressive.

How much is a SS check for the average MD? Here we can expect 1000€/month at age 67...

Not badI believe max SS check is about 3 grand a month these days

I got this figure from a family friend who is a physician (thus contributing max to SS throughout his career) and waited the longest before collecting SS (either 67 or 70 yrs old- I forgot)Not bad

A buddy of mine just retired at 63 with $2mil, mortgage paid off, never divorced, and kids out of college. He is loving life and has plenty of money as long as he doesn't go crazy.

My game plan is also to go part time some point in the distant future (once loans/mortgage is paid off, etc), rather than going from full time employment straight into complete retirement. Seems like in the right scenario, you could keep up your skills in case you later on decide you want/need to work more. I don't think I need 100% free time to have what I would consider to be a high-quality life.

I'm a conservative investor who has a nice retirement fund already. I like working but am looking for a less hectic job. Still, my goal is $10 million so I can comfortably leave $3 million to my children once I'm gone. My life expectancy is likely 82-85 based on family history and current health. Of course, I could die tomorrow but the life insurance combined with my current savings would leave my wife and kids financially secure. This gives me peace of mind.

My wealth isn't about fancy cars or expensive items. In fact, I live frugally compared to some others on SDN who have 1/4 my assets. The money means security and the option of walking away at any moment of my choosing. I CHOOSE to work because I want to and not because I have to. That really changes your mind set about the job and work/life balance.

If I was a new grad in this environment I'd probably just plan for $4 million then look at all my options. I think a new grad could save up $4 million by age 65 with a little effort and restraint.

Compound Interest Calculator

Compound Interest Calculator | Investor.gov

I am pretty far from retirement so pardon my ignorance, but doesn’t the IRS require a minimum withdrawal amount from your accounts once you reach a certain age or you risk being penalized? I believe this is called the required minimum distribution. Does that need to factor into the dollar amount needed for retirement?

I am pretty far from retirement so pardon my ignorance, but doesn’t the IRS require a minimum withdrawal amount from your accounts once you reach a certain age or you risk being penalized? I believe this is called the required minimum distribution. Does that need to factor into the dollar amount needed for retirement?

Is this the magic number needed to retire at any age from medicine and say F it all?

What is everyone's magic number to get out?

On $4 million the RMD is $146,000. That's just over 3.5% but likely some of your nest egg at age 70.5 won't be in an IRA. Typically, high income wage earners have savings outside their IRA/401K. For me, it's 2/3 (outside) vs 1/3 (IRA/401k). I expect the opposite for a new grad today working as an employee (2/3 IRA/401K and 1/3 personal investments).

Minimum IRA Distribution Calculator: What Is My Minimum Required IRA Distribution?

IRA Required Minimum Distributions Table

How can you tell that? I am reading about 10-40 million dollar lawsuits almost weekly these days against physicians.

This is the most recent one: Torture death of 8-year-old Gizzell Ford leads to $48M jury award over doctor missteps

Unless you directly work for the county who assumes all liability, what happens when you get a 48M judgement against you? The plantiff lawyers just walk away at 1M insurance?

Also, Texas offers unlimited Homestead but who wants to put all their assets into a home?

I wonder if the ratio might be the opposite for new grads. Many new grads are employed positions with no match, so tax deferred savings is limited. I think many new grads should plan to have the majority of their savings in a taxable account. 18k in a 401k and 5.5k in a backdoor Roth is nowhere close to enough savings considering the debt and late start.