More Q&A

Your blog and your strategy inspires me! Appreciate for your sincere advises and feedback so far, Dr. Amanda Liu! Please, use our discussion on your blog

🙂 I emailed to Alex, by the way. Let me know if I can help you further. Also, I asked him if I can re-apply with expected PGY1 income. I tried to reapply online but I couldn't b/c I was already rejected with $0 income input on my previous application...Maybe I should call DRB tomorrow. Is there an adviser or person you would recommend me to talk to in DRB? Is it better to stay on fixed or variable interest rate when refinancing?

If you were me with $206,400 principle from all med school only ($21,386 interest, currently) with avg. 6.08%, which option would you go with personally? From your voice, it sounds like you will definitely go with refi and use the cash flow into retirement savings account. If I go with this refi route, is it more beneficial for me to use the cash flow to pay more monthly for student loans or making minimum monthly/putting cash flow into retirement savings/emergency funds? OR, maybe I can pursue both which is doable during my 6 yrs training?

Can you briefly explain when and how I can start investing into IRA ROTH and company match? Do you recommend to start opening account starting at PGY1?

With your big help so far, I narrowed down to two choices as below with

my goal for the loan repayment option (

have the option that provides me the most minimum monthly repayment so I can have more flexibility or room to pay more if I choose to with less interest rate; pay off completely within 2-3 yrs of post-residency training):

1)

Refi with DRB now (if approved) for 6 yrs and then re-Refi when becoming attending

- Is it worth a lot if I refi now from 6.08% to 4.5% using DRB? Is 4.5% under 10 yrs plan guaranteed most of time when I apply, recently?

- Under this plan, you mentioned I can keep re-refinance. Is there a penalty from DRB (assumed I refi with them), when I refi again after 6 yrs (when I get a job) to different bank?

- From your comments above, you mentioned that someone was approved for 4.5%, but fed interest rate of 7% is still alive? This didn't make sense to me. If refi worked, fed interest rate should go away and that person will be locked in with 4.5% right after he was approved as a fixed rate, no?

2)

PAYE(or RePAYE) with PSLF for 6 yrs and then re-Refi when becoming attending

- I totally agree with you that PSLF is not going to help us (Radiology) much. But, based on your wisdom, I might as well apply to PSLF (if I have to choose one of IDRs) since it won't do me any harm even if I will get my 1st job at the profit organization which most rads people get.

- Out of other IDRs options, if you were to choose one of IDR with my mentality and will to make extra monthly payment, would you still go with RePAYE over PAYE due to interest subsidy? If I can make extra monthly, I think being on either of these PAYE vs. RePAYE won't be matter, right? I mean it will be ideal if I pay the most minimum under RePAYE to get the most benefit, but now I feel like being on RePAYE won't hurt me neither if I choose to pay more monthly (close to interest accrued) ~$1100/month.

- When I switch from PAYE (or RePAYE) to refi after 6 yrs, unpaid interests during these 6 yrs will be capitalized and these total amount will be refinanced, correct?

- If I go with either of PAYE vs RePAYE, will Direct consolidation provide me lower rate than current average rate of 6.08%? I will ask the lender this question, also.

It is awesome to see that you are a 1st yr rad at UofA!! I went to undergrad there. Currently, I just finished all of my clinical rotations here at Phoenix before graduation in May. I am going to Univ Nevada at Reno for my medicine internship this year and Univ Texas at Houston for my radiology training starting next year. Where did you do your intern year? Anyhow, I am so glad to bump into you here at SDN especially when I meet someone like you who really understands my dilemma and concerns over this student loan issue! Thank you for your big help!!!

--

DWM response:

Your blog and your strategy inspires me! Appreciate for your sincere advises and feedback so far! I can re-apply with expected PGY1 income. I tried to reapply online but I couldn't b/c I was already rejected with $0 income input on my previous application...Maybe I should call DRB tomorrow. Is there an adviser or person you would recommend me to talk to in DRB? Is it better to stay on fixed or variable interest rate when refinancing?

If you were me with $206,400 principle from all med school only ($21,386 interest, currently) with avg. 6.08%, which option would you go with personally? From your voice, it sounds like you will definitely go with refi and use the cash flow into retirement savings account. If I go with this refi route, is it more beneficial for me to use the cash flow to pay more monthly for student loans or making minimum monthly/putting cash flow into retirement savings/emergency funds? OR, maybe I can pursue both which is doable during my 6 yrs training?

Can you briefly explain when and how I can start investing into IRA ROTH and company match? Do you recommend to start opening account starting at PGY1?

With your big help so far, I narrowed down to two choices as below with

my goal for the loan repayment option (

have the option that provides me the most minimum monthly repayment so I can have more flexibility or room to pay more if I choose to with less interest rate; pay off completely within 2-3 yrs of post-residency training):

1)

Refi with DRB now (if approved) for 6 yrs and then re-Refi when becoming attending

- Is it worth a lot if I refi now from 6.08% to 4.5% using DRB? Is 4.5% under 10 yrs plan guaranteed most of time when I apply, recently?

- Under this plan, you mentioned I can keep re-refinance. Is there a penalty from DRB (assumed I refi with them), when I refi again after 6 yrs (when I get a job) to different bank?

- From your comments above, you mentioned that someone was approved for 4.5%, but fed interest rate of 7% is still alive? This didn't make sense to me. If refi worked, fed interest rate should go away and that person will be locked in with 4.5% right after he was approved as a fixed rate, no?

2)

PAYE(or RePAYE) with PSLF for 6 yrs and then re-Refi when becoming attending

- I totally agree with you that PSLF is not going to help us (Radiology) much. But, based on your wisdom, I might as well apply to PSLF (if I have to choose one of IDRs) since it won't do me any harm even if I will get my 1st job at the profit organization which most rads people get.

- Out of other IDRs options, if you were to choose one of IDR with my mentality and will to make extra monthly payment, would you still go with RePAYE over PAYE due to interest subsidy? If I can make extra monthly, I think being on either of these PAYE vs. RePAYE won't be matter, right? I mean it will be ideal if I pay the most minimum under RePAYE to get the most benefit, but now I feel like being on RePAYE won't hurt me neither if I choose to pay more monthly (close to interest accrued) ~$1100/month.

- When I switch from PAYE (or RePAYE) to refi after 6 yrs, unpaid interests during these 6 yrs will be capitalized and these total amount will be refinanced, correct?

- If I go with either of PAYE vs RePAYE, will Direct consolidation provide me lower rate than current average rate of 6.08%? I will ask the lender this question, also.

It is awesome to see that you are a 1st yr rad at UofA!! I went to undergrad there. Currently, I just finished all of my clinical rotations here at Phoenix before graduation in May. I am going to Univ Nevada at Reno for my medicine internship this year and Univ Texas at Houston for my radiology training starting next year. Where did you do your intern year? Anyhow, I am so glad to bump into you here at SDN especially when I meet someone like you who really understands my dilemma and concerns over this student loan issue! Thank you for your big help!!!

--

DWM response:

I tried to reapply online but I couldn't b/c I was already rejected with $0 income input on my previous application.

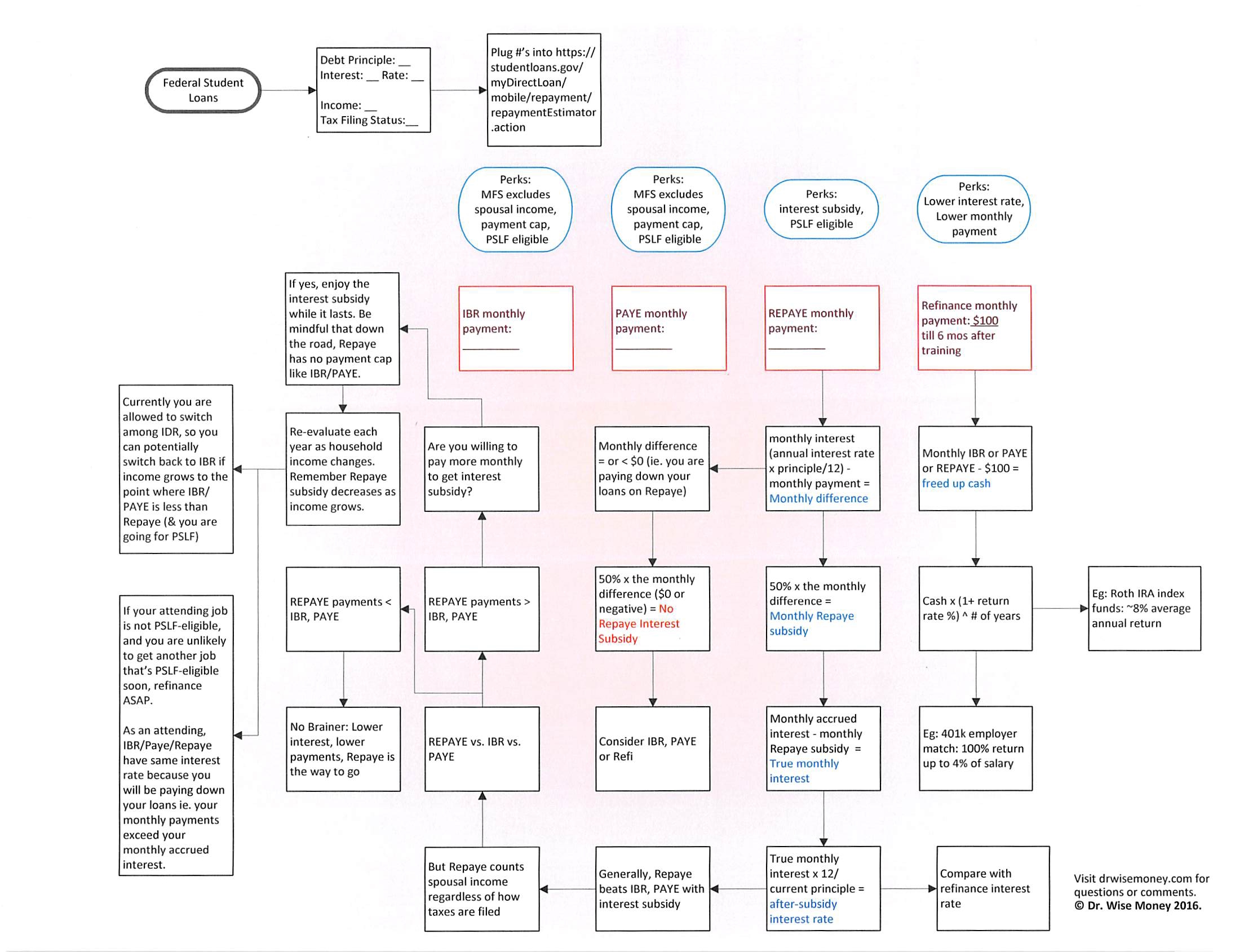

Definitely call DRB tomorrow and have them manually change your income so that your application will reflect your PGY 1 rather than your MS4 income. One of the big benefit DRB advertises is the fact that they go one step further than refinancing PGY’s, that they will refinance MS4 with contract in hand after match day.

Is there an adviser or person you would recommend me to talk to in DRB?

I was rejected by DRB when I applied for student loan refinancing as an intern. That was before they started offering student loan refinancing for residents and fellows. I worked with Jason, who really knew his stuff, but I felt so frustrated because their rules back then was that you had to have $3,500/mo. after paying all your bills to be even considered, even though I had 800+ credit score. But I’m really glad to see that many of my friends are able to take advantage of student loan refinancing as PGY’s now after DRB started offering PGY refinancing in mid-2015.

Is it better to stay on fixed or variable interest rate when refinancing?

Since you are at the beginning of your training, I’d recommend staying with fixed rate. However, you can always re-refinance again if you selected variable interest rate right now and the rate went up. You can refinance your loans with DRB with DRB again or with LinkCapital (hopefully they are able raise capital and start refinancing PGY’s again.)

For example, if you refinance with DRB right now and got a much lower variable rate than you would if you select fixed interest rate under the same 10 year long term, and in 2 years, the rate went up by 1%, and you really don’t like the new rate. Then you can apply to LinkCapital for either a fixed or variable rate interest loan. If LinkCapital offers you good deal, then you can bring the deal back to DRB, ask DRB if they want to beat the deal from LC, then they can keep your business.

The only downside to selecting variable rate & re-refinancing if rate increases and starts cutting into your savings are:

1. No one can really predict how rates will go. Yes federal government is increasing the prime interest rate where banks can borrow money gradually, already by 0.25% this year. But if economy sucks, like it sort of does now, the interest rate of refinancing student loans and mortgage, etc. will stay low.

2. There are only 2 banks offering PGY refinancing right now, and one of them LC is out of money to lend/currently in the process of trying to raise more money. So DRB pretty much has total monopoly of the PGY student loan refinancing market right now! Great position for DRB to be in, not the best for the PGY’s who need these refinanced student loans to save money. So if your variable interest rate increases with DRB, and there’s only LC (assuming they get enough money and start lending to PGY’s again), then you may not get a great deal when you re-refinance.

So it is personal decision whether to refinance to variable or fixed but in general, variable rate is fantastic when interest rate drifts down from the time when you sign up rather than drift up. But no one can count on a borrower-favoring downward trend just as banks can’t count on a lender-favoring upward trend. What you need to do is to consider the worst case scenario: If your variable interest rate goes up, and you cannot get out that high interest rate by re-refinancing, what can you do? If you are an attending, you can probably pay off your student loans rapidly, within a year or two by just tightening your belt a bit or re-refinance, but if you are PGY, you may be stuck with the high inter rate until it adjusts down (economy down turn, federal government decreases prime rate, etc.) or when you get to refinance again as an attending.

If you were me with $206,400 principle from all med school only ($21,386 interest, currently) with avg. 6.08%, which option would you go with personally?

I would refinance because I don’t like debt. I will choose a 7 year or 10 year fixed interest rate loan. I’d imagine that my rate will be around 4.5% or so. Even if it is 5%, I’d still refinance because I will be very aggressive with paying down my student loan throughout training (since our training is so long, 6 years.)

From your voice, it sounds like you will definitely go with refi and use the cash flow into retirement savings account. If I go with this refi route, is it more beneficial for me to use the cash flow to pay more monthly for student loans or making minimum monthly/putting cash flow into retirement savings/emergency funds?

I will

1. Make a budget and see how much money I can allocate to building my net worth by decreasing debts and increasing assets.

2. As an intern, I was targeting $2000/mo. towards increasing my net worth. I focused on attacking my student loans first because my interest rate was 6.8%. I was very happy to throw $2000/mo. towards my student loans and every extra penny I had towards them because I knew I was making 6.8% return on every dollar I used to pay down my loans.

3. As soon as I killed my student loans, I started to max out my retirement funds, which means to max out both Roth IRA and 403b Roth at BUMC, a total of 23.5k/year.

OR, maybe I can pursue both which is doable during my 6 yrs training?

Yes, you can definitely do both. Whether you decrease your debts or increase your assets (saving more in retirement accounts), you are increase your net worth.

Can you briefly explain when and how I can start investing into Roth IRA and company match?

Read these posts.

http://drwisemoney.com/?s=bitter+sweet

http://drwisemoney.com/2016/01/27/where-to-put-limited-pgy-dollars/

http://drwisemoney.com/?s=company+match

http://drwisemoney.com/2015/12/12/christmas-a-gift-that-keeps-on-giving/

For company match, contact your hospital HR/benefits department to find out if they offer residents/fellows a match. If they do, definitely open a 401k or 403b account to take advantage of the match. UA did not use to offer company match for retirement savings, but thankfully Banner bought UA and starts offering 4% company match on 7/1/2016 for PGYs. So yay, that’s another 2-4k/year of money one can get by putting away 2-4k themselves into their 401k.

Do you recommend to start opening account starting at PGY1?

Yes, definitely start Roth IRA

ASAP. You can read this post and learned from my biggest mistake J I would have started Roth IRA in medical school if I knew how wonderful Roth IRA savings are.

http://whitecoatinvestor.com/hitting-a-net-worth-of-0-as-an-intern/

With your big help so far, I narrowed down to two choices as below with

my goal for the loan repayment option (

have the option that provides me the most minimum monthly repayment so I can have more flexibility or room to pay more if I choose to with less interest rate; pay off completely within 2-3 yrs of post-residency training):

1)

Refi with DRB now (if approved) for 6 yrs and then re-Refi when becoming attending

- Is it worth a lot if I refi now from 6.08% to 4.5% using DRB?

So rough math is 228k x (6.08% - 4.5%) x 6 years of training

= $20,520 guaranteed post tax savings even if you choose to pay nothing like in the case of $0 monthly requirement by LC.

That’s about half a year of post-tax income as a PGY1. I think it’s a big deal, but others may think differently.

- Is 4.5% under 10 yrs plan guaranteed most of time when I apply, recently?

No, not guaranteed. Could be higher or lower. Apply for free and find out.

- Under this plan, you mentioned I can keep re-refinance. Is there a penalty from DRB (assumed I refi with them), when I refi again after 6 yrs (when I get a job) to different bank?

DRB currently has NO pre-pay penalty; you can refinance with anyone that wants your business.

- From your comments above, you mentioned that someone was approved for 4.5%, but fed interest rate of 7% is still alive?

My colleague signed the paper agreeing to have DRB buy his loans from the federal government, who’s charging him 7% currently. However, DRB has been really slow at moving forward. They are probably getting too much business. That’s why I recommend that anyone who is even considering refinancing to apply ASAP, because the borrower can get the DRB deal in hand first and still have time to think about the best course of action, After learning what rates/terms DRB will offer the specific borrower.

This didn't make sense to me. If refi worked, fed interest rate should go away and that person will be locked in with 4.5% right after he was approved as a fixed rate, no?

You are totally right. As soon as DRB go ahead and buy the student loans from the federal government, my friend is set on his fixed 4.5% interest rate until the end of his selected term (I believe he selected 7 year term because he is a pgy3.)

2)

PAYE(or RePAYE) with PSLF for 6 yrs and then re-Refi when becoming attending

- I totally agree with you that PSLF is not going to help us (higher paying specialties) much. But, based on your wisdom, I might as well apply to PSLF (if I have to choose one of IDRs) since it won't do me any harm even if I will get my 1st job at the profit organization which most rads people get.

Yes staying with IDR/PSLF combination only hurts you

if your interest rate on IDR is higher than that of refinancing with private banks.

- Out of other IDRs options, if you were to choose one of IDR with my mentality and will to make extra monthly payment, would you still go with RePAYE over PAYE due to interest subsidy?

If I plan to pay minimum, I’d stick with RePAYE so I can get maximum interest subsidy.

If I can make extra monthly, I think being on either of these PAYE vs. RePAYE won't be matter, right?

If I plan to pay anywhere close to the monthly accrued interest, causing nearly $0/mo. interest subsidy on RePAYE, then I’d go with PAYE. I am saying this because RePAYE beats other plan like DRB/PAYE by interest subsidy. On the other than IBR/PAYE beats RePAYE by 2 things that may become relevant to you in the future:

1. IBR/PAYE will not count spousal income as long as you file taxes separately. (RePAYE counts spousal income always no matter how you file taxes.)

2. IBR/PAYE lifetime maximum payment requirement is capped by the monthly payment you get under standard 10 year repayment plan at the time you enroll with IBR/PAYE. (RePAYE has no payment cap, so you can potentially make enough money as an attending that your monthly RePAYE requirement gets higher than monthly IBR/PAYE requirement.

However, these 2 issues make no difference to someone who’s paying down their student loans aggressively rather than paying the monthly IDR plan requirement waiting for PSLF. But since you don’t know for sure that you won’t get PSLF, IBR/PAYE are better than RePAYE.

I mean it will be ideal if I pay the most minimum under RePAYE to get the most benefit, but now I feel like being on RePAYE won't hurt me neither if I choose to pay more monthly (close to interest accrued) ~$1100/month.

RePAYE won’t hurt you as long as

1. You can switch back to IBR/PAYE, when you the above mentioned 2 points are relevant to you and that you’d rather pay less on IBR/PAYE so that you get More forgiven under PSLF.

2. If you don’t get a PSLF-eligible job and you are going to pay off your debt yourself ASAP anyways, you can just refinance from RePAYE to a private bank and destroy your debt within 2-4 years after training.

- When I switch from PAYE (or RePAYE) to refi after 6 yrs, unpaid interests during these 6 yrs will be capitalized and these total amount will be refinanced, correct?

Yes. When you finish training, you will no longer qualify for PAYE because you no longer demonstrate partial financial hardship. When you leave PAYE either voluntarily or due to non-qualification, your interest will capitalize too. Interest will capitalize whether you get automatically switched from PAYE to standard 10 year repayment or you refinance.

- If I go with either of PAYE vs RePAYE, will Direct consolidation provide me lower rate than current average rate of 6.08%?

No, Direct consolidation loan is usually 1/8% higher than your current weighted interest rate, so your rate will likely be 6.125% instead of 6.08%. You can confirm this with your servicer. The only reason people consolidate is to make sure that All of their federal government loans become PSLF-eligible. But if all your current individual loans are Direct; they are all PSLF-eligible already. Federal loans like Grad Plus loans are not PSLF-eligible, so a borrower with Grad Plus loans should probably consolidate.

It is awesome to see that you are a 1st yr rad at UofA!! I went to undergrad there. Currently, I just finished all of my clinical rotations here at Phoenix before graduation in May. I am going to Univ Nevada at Reno for my medicine internship this year and Univ Texas at Houston for my radiology training starting next year.

Where did you do your intern year?

U of A too. It was important to me that I can do all my PGY in the same place and not move my family around again.

Anyhow, I am so glad to bump into you here at SDN especially when I meet someone like you who really understands my dilemma and concerns over this student loan issue! Thank you for your big help!!!

My pleasure.