By David Enna, Tipswatch.com U.S. Series I Savings Bonds are a unique investment because all interest is rolled into principal until redemption, and in most cases, all the compounded earnings are t…

tipswatch.com

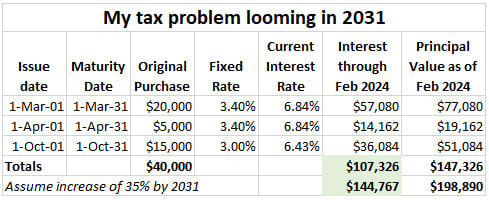

FYI. A warning for those thinking of purchasing paper I-bonds

"My bank (Wells Fargo in Charlotte) still redeems paper savings bonds, but some banks no longer offer that service. TreasuryDirect says, “Banks vary in how much they will cash at one time – or if they cash savings bonds at all.” From a recent New York Times (

When Did Cashing Savings Bonds Become So Impossible?) article:

Hoping to cash in a paper savings bond that’s been lying around for a few decades? Set aside a lot of time for disappointment. …

The process is only getting harder. In May, the nation’s largest bank, JPMorgan Chase, began imposing a $500 limit on each savings bond cashed for longtime depositors — that’s total redemption value, so including any interest owed. Wells Fargo and Citi place a $1,000 limit on new customers. U.S. Bank has

a five-year waiting period before it will cash a bond for a new customer."

. Good Luck.

. Good Luck.