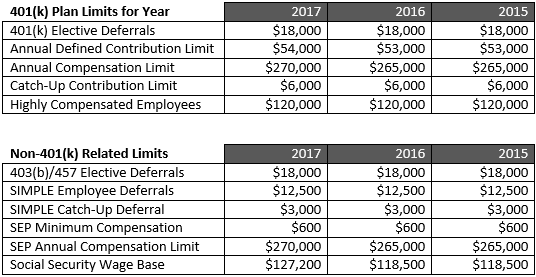

PGG is correct about the fact that it is what you keep after expenses/living that matters to grow wealth. But, what he doesn't understand or explain well is the tax code is set up to hurt the little guy. Currently, maximizing the 401K ($54,000 per year) is the BEST WAY for any Physician to obtain wealth over 3 decades. Hence, I'd advise against taking jobs which deny you the option of tax deferral unless the compensation reflects this significant hit to your bottom line.

Independent groups and 1099 employment allow an individual to use the tax code in a much more efficient manner. Unfortunately, the vast majority of jobs are dead end types with poor retirement plans.

"However, the truth is that for most physicians, the very best place to invest their next dollar is inside a tax-deferred retirement account such their employer’s 401(k), 403(b), defined benefit/cash balance plan, or even 457(b), and in the case of a self-employed physician, an individual 401(k) or cash balance plan."

Tax-deferred Retirement Accounts: A Gift from the Government

")