Time to rebalance the portfolio.

When is it not? Nearly everybody should have a portfolio that is rebalancing on some annual or semiannual basis.

Once a year at least.

Time to rebalance the portfolio.

People are flocking to gold and bonds for safety.

Gold is up 4%

When everybody is heading one way, the smart play in the long term is usually the other way. Bubbles burst when everybody and their brother is buying because something is up so high. Similarly the end of a bottom is near when everybody seems to want out.

Contrarians to hugely popular sentiment have a history of performing very well in the investment world over the long haul.

Exactly. Once we get below 12000... I'll start putting a little back into the market. Below 11000 alot more. @ 9000, I'm (almost) all in.

When is it not? Nearly everybody should have a portfolio that is rebalancing on some annual or semiannual basis.

Once a year at least.

Or when predetermined threshholds have been met. Not quite there yet.

When? Another 3 percent down? Some say 1202 on the S and P. I'm buying just a little further down from here. 3 percent more. I'd like 5 percent just to be safe but I'll deploy cash at 1230 and more if we go below 1200 (s and p)

I believe the next technical support is 1202.

Anecdotal. Was talking to a friend of mine the other day. CT Anesthesiologist. Golden schooling, name school, name residency, name fellowship, amazingly nice guy. I visited his house couple years ago, spent a week in OR with him.

At that time, 2009, he told me he was making $600,000+. Right in that range. Seemed like the dream job, PP, great hospital, respect, autonomy, great partners, covering 4 rooms with partners, FAST surgeons (1/2 time as other places I've shadowed to do CABG etc). He was HAPPY.

Cut to, 2012, a week ago, I was talking to him about my career dilemma etc. Mentioned that he was making $450,000 this year. I did a double take, what happened to 6 plus I asked? Had I heard that wrong. Nope, less reimbursements, hospital subsidy slowly going away. Bla bla bla. $450,000 is still bank, but, fairly, it's not $600,000.

Cut to 2020, when I'd graduate. His opinion is he'll be making ~$250,000, who knows what a new grad will be making. $250,000 is still a lot of money. but it's not $450,000.

And it's not $600,000.

This guy is the polar opposite of gloom and doom, as much as I am. He was trying to cut it straight to me, as a friend.

I don't like hearing that from a really great, straight shooting guy. About the profession. Thought I'd share. Blade's been calling this, with others, for the longest time. Frustrating. It's happening...

D712

Sorry, but I call it as I see it. The income will level out in a similar manner to ER medicine. In some respects, we will become more like ER docs in the sense of hospital or AMC employment, shift work, more delegation to others like CRNAs and of course, lower reimbursement.

The full transition will take another 6-10 years. The time frame depends more on ObamaCare (SCOTUS ruling at the end of June) and who wins the White House in November. We still end up in the same place ($300K) but I'm hoping later rather than sooner.

Owning Gold as part of a diversified portfolio makes sense. You now have opportunity to buy Gold soon at under $1500 an ounce. I will be a buyer of Gold again at that price and all over Platinum at $1450 or less (could be this week).

Use common sense. Look at the long term value of US paper currency vs US Gold Coins or GLD as ask yourself which is a better way to hold cash. That's right CASH. MY Gold Coins are US currency just like your paper money but the US mint simply can't print all the Gold coin the Fed tells them to.

Blade, are you still advocating fellowships the way you have before?

I believe a fellowship is more essential now than anytime in the specialty's history.

What fellowships are best to pursue? Critical care? Pain?

The one you enjoy doing the most

Oh, sure. But I mean within the context of this discussion. What fellowships make Anesthesiologists the most marketable going forward?

rebalancing bands: I use the 5/25 rule. e.g, if you are 60/40 stock bonds, if the market drops sell bonds when you are 55/45. Or if using multi asset classs investing say you have 10% REITs. rebalance back down to 10% if they become 12.5% of portfolio and rebalnce up when they hit 7.5% of portfolio.

Dude. Great posts. I think you mentioned a rebalancing band before we took the recent dive. Kudos. 👍

If we stay at this downward pace....

Blade, what fields in medicine do you think will make it out least scathed by the ACA over the next 5-10 yrs?

Blade, what fields in medicine do you think will make it out least scathed by the ACA over the next 5-10 yrs?

I expect a relief rally in December as a short term deal is reached. The market will likely get near 52 week highs. I'm a seller of volatile equities and funds for 2013. I'm moving into "Doze" style funds and investment style.

I think slow growth at best in 2013, tax hikes, more regulation and significant Medicare cuts to physicians going forward (grand bargain results in cuts starting in 2014).

My outlook for the country's future looks bleak. The strategy of solid, consistent, dividend paying stocks in the U.S. combined with good emerging market companies seems like a nice strategy. I will be using ETFs or Vanguard funds to invest going forward (already moved a good sum there). Doze is correct on that count as well.

As for my bond funds I'm sticking with Short term funds and maybe some intermediate funds for the next few years. I'm decreasing my stake in equities as part of my early retirement strategy.

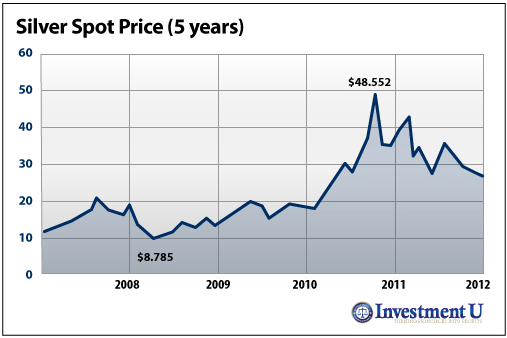

I still like Gold, Silver and Precious metals under an Obama administration that will print as much money as Congress allows.

Real Estate looks good going forward as well both domestic and international. Again, being diversified here by using ETFs or Funds is wise decision.

Last but not least is an Iran vs Israel conflict in 2013. I'd say that is 50/50 and such a conflict will raise gasoline prices and depress the stock market. Israel isn't likely to win such a conflict.

The one issue with real estate if you are using REITs is if the interest rates go up, you can really get creamed with REITs. Same with the bond market. Unfortunately, I don't have a crystal ball to predict when this will happen.

I expect a relief rally in December as a short term deal is reached. The market will likely get near 52 week highs. I'm a seller of volatile equities and funds for 2013. I'm moving into "Doze" style funds and investment style.

I think slow growth at best in 2013, tax hikes, more regulation and significant Medicare cuts to physicians going forward (grand bargain results in cuts starting in 2014).

My outlook for the country's future looks bleak. The strategy of solid, consistent, dividend paying stocks in the U.S. combined with good emerging market companies seems like a nice strategy. I will be using ETFs or Vanguard funds to invest going forward (already moved a good sum there). Doze is correct on that count as well.

As for my bond funds I'm sticking with Short term funds and maybe some intermediate funds for the next few years. I'm decreasing my stake in equities as part of my early retirement strategy.

I still like Gold, Silver and Precious metals under an Obama administration that will print as much money as Congress allows.

Real Estate looks good going forward as well both domestic and international. Again, being diversified here by using ETFs or Funds is wise decision.

Last but not least is an Iran vs Israel conflict in 2013. I'd say that is 50/50 and such a conflict will raise gasoline prices and depress the stock market. Israel isn't likely to win such a conflict.

FWIW, in this market (and mortgage rates), we are getting a second vacation home as a means to diversify and use it as short term rental income. Looks like the housing market has bounced off the bottom a little, but plenty of good property on sale.

I expect a relief rally in December as a short term deal is reached. The market will likely get near 52 week highs. I'm a seller of volatile equities and funds for 2013. I'm moving into "Doze" style funds and investment style.

I think slow growth at best in 2013, tax hikes, more regulation and significant Medicare cuts to physicians going forward (grand bargain results in cuts starting in 2014).

My outlook for the country's future looks bleak. The strategy of solid, consistent, dividend paying stocks in the U.S. combined with good emerging market companies seems like a nice strategy. I will be using ETFs or Vanguard funds to invest going forward (already moved a good sum there). Doze is correct on that count as well.

As for my bond funds I'm sticking with Short term funds and maybe some intermediate funds for the next few years. I'm decreasing my stake in equities as part of my early retirement strategy.

I still like Gold, Silver and Precious metals under an Obama administration that will print as much money as Congress allows.

Real Estate looks good going forward as well both domestic and international. Again, being diversified here by using ETFs or Funds is wise decision.

Last but not least is an Iran vs Israel conflict in 2013. I'd say that is 50/50 and such a conflict will raise gasoline prices and depress the stock market. Israel isn't likely to win such a conflict.

What do you think will happen to residential real estate prices when interest rates rise (and they must at some point; mortgages can't sit at 3-4% forever) and the amount of home a family can "afford" drops because what they can "afford" is based on monthly payment and not home price?

This isn't the bottom of the market. The house you buy today for $X at 3.25% won't sell for $1.1X at 6-7% in 10 years. A couple decades ago, mortgage rates of 9% were good. These artificially low rates are tremendously distorting to home prices.

If you're buying a house to rent and have positive cash flow on it from day 1, great, but if you're buying now expecting it to beat inflation over the next couple decades (which is a tall order for real estate held long in the first place) I think you'll be disappointed. That doesn't mean you can't enjoy your 2nd home, and if this is a luxury property in a resort area the market forces may well be different. Real estate is all about location, of course.

Only my opinion of course. 🙂

There is a certain place in the Rocky Mountains I'm totally in love with.

Does this mean you're going to bail on Apple before it hits 900? 😀

Stay short and high quality on your bonds.

-More money has been lost reaching for yield than at the point of a gun. (I forget who said it)

REITs are not bonds. They can and do drop 50% over short time periods.

There is some funny business going on in the REIT market. As investors are desperate for yield and REITs are obligated to pay the lion's share of their profits as dividneds- Many companies that are not traditional REIT industries- (apts, office buildings, strip malls) are converting to a REIT structure-for the sole intention of boosting the company's market cap. THis may change their value as a diversifier in a portfolio.

I'm invested in the muni fund we discussed via PM. I hope the Democrats don't tax my muni bond income in 2013. I'm hearing rumors that my muni bonds may become taxable income😱

That place is beautiful. More pictures will be expected when you find a place!