You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Recommend me a stock.

Started by urge

Best stocks are probably the ones most people haven't already heard of. I don't think Tesla fits, since it's already world famous, though they'll continue to do well as a company. But if you can afford the current almost $350 price . . . .This is not a how to invest thread.

This is a place to recommend a stock that you think will do well.

We know some folks like Pacira, Cipotle, etc.

What other stocks do we like?

I'll start: Tesla

Why? Self driving trucks in the horizon.

If you like Elon Musk, and think there's money to be made in his vision of space exploration, then at least SpaceX is still private and hasn't had their IPO.

Last edited:

D

deleted50478

Best stocks are probably the ones most people haven't already heard of. I don't think Tesla fits, since it's already world famous, though they'll continue to do well as a company. But if you can afford the current almost $350 price . . . .

If you like Elon Musk, and think there's money to be made in his vision of space exploration, then at least SpaceX is still private and hasn't had their IPO.

Tesla has a larger market cap than GM despite selling less than 1% as many cars. I don't doubt they'll gain market share but it seems to me their success is already priced in with limited upside and significant potential downside. That could be wrong though. Maybe they'll be bigger than Toyota in 10 years but that's pretty optimistic with so many established manufacturers releasing electric vehicles in the next few years.

I hope they are that successful but I won't be betting too much of my money on it.

Advertisement - Members don't see this ad

D

deleted126335

Don't pick individual stocks.

If I had to pick an asset class to hold for a decade or more that would be emerging markets. Usual caveats.

VWO is fine.

If I had to pick an asset class to hold for a decade or more that would be emerging markets. Usual caveats.

VWO is fine.

If you are willing to take a risk and you think oil will be $60/barrel again within two years, there are lots of companies in the oil patch selling at bargain prices. Offshore drilling in particular has been hit hard. All of the offshore drillers have about half their rigs sitting idle, and the contracts they sign nowadays are at or below breakeven prices. It could be years before they bring in the kind of money they made in 2013, but when oil goes up those stocks are going to explode. RIG, ESV, RDC, DO and NE are the five companies most likely to survive the downturn. HOS, an offshore service company, is an even more speculative bet as they’ll be the last in line to get paid, but their stock is dirt cheap right now.

If you want to invest in any of those companies, make sure you do your homework. Some are going through mergers, others have excessive debt, others have a large pool of obsolete rigs that will never work again. This is a risky, but potentially rewarding sector to invest in.

Disclosure: Long ESV, DO, HOS

If you want to invest in any of those companies, make sure you do your homework. Some are going through mergers, others have excessive debt, others have a large pool of obsolete rigs that will never work again. This is a risky, but potentially rewarding sector to invest in.

Disclosure: Long ESV, DO, HOS

Chipotle

We will check this thread in 10 years and see how we did.Tesla has a larger market cap than GM despite selling less than 1% as many cars. I don't doubt they'll gain market share but it seems to me their success is already priced in with limited upside and significant potential downside. That could be wrong though. Maybe they'll be bigger than Toyota in 10 years but that's pretty optimistic with so many established manufacturers releasing electric vehicles in the next few years.

I hope they are that successful but I won't be betting too much of my money on it.

Don't pick individual stocks.

If I had to pick an asset class to hold for a decade or more that would be emerging markets. Usual caveats.

VWO is fine.

Why?

Besides the recent run, emergent markets have struggled for a very long time.

Comparing emerging markets to our total stock market shows a huge difference in returns over 10 years (favoring US total stock market etfs).

Just curious as to your thinking.

Do you believe them to be undervalued?

Just curious as to your thinking.

Do you believe them to be undervalued?

D

deleted126335

Comparing emerging markets to our total stock market shows a huge difference in returns over 10 years (favoring US total stock market etfs).

Just curious as to your thinking.

Do you believe them to be undervalued?

They certainly are cheaper than US markets.

Future expected returns are based on current valuations, expected growth rates, and historical pricing. Given that expected growth rates for EM are as least as good as the US and they are a helluva lot cheaper, they are expected but not guaranteed to outperform going forward. If you wanna get fancy go for EM Value as value has underperformed growth for awhile. dfevx, fnde, or pxh.

While I value tilt, I don't change allocation based on market valuation levels. Other than lowering my overall equity allocation as I get closer to winning the game.

Advertisement - Members don't see this ad

Chipotle

PE is 63. It's still priced like a growth company, but it's not growing.

I wanted to invest a few years ago when they announced ShopHouse and Pizzeria Locale, but I wanted to see those gain some traction. Looks like they shut down ShopHouse. Only 3 locations so far for PL. Looks like dead money for now.

Whoever develops and sells eCigs (?)

D

deleted162650

Figure out who the big players in marijuana will be over these next couple years. Some people are gonna make fortunes up until it's legalized in enough states/federally that Philip Morris will step in, buy them out, and own pot just like they own tobacco.

.

Facebook

Comparing emerging markets to our total stock market shows a huge difference in returns over 10 years (favoring US total stock market etfs).

Just curious as to your thinking.

Do you believe them to be undervalued?

Yes. It is known as "reversion to the mean" and at some point (which I believe is now) the emerging markets will go on a multi-year run with double digit returns.

My asset allocation since last year has tilted towards foreign equities and emerging markets (overweight in these areas relative to my normal allocation) with outstanding results so far.

If you already have a modest dose of international equities in your portfolio, increasing that percentage could make sense for the next decade. Research by Vanguard shows that keeping 40% of your stock portfolio in foreign shares offers the best balance of risk, return, and diversification.

If you don’t want to constantly worry about what percentage of your equity portfolio to keep in international shares, consider a global fund like Vanguard Total World ETF ( VT) . You’ll get a sampling of the entire world’s stock markets—including the U.S.—for just 0.14% in expenses a year. The fund currently has about 45% of its assets in international stocks, and seven percentage points of that

is in the emerging markets.

If you simply want international exposure, it’s hard to argue with Vanguard All-World ex-U.S. ETF ( VEU) , which charges just 0.13% a year. In addition to investing about 15% directly in emerging-markets stocks, this Vanguard fund has as its biggest holding Nestlé, the Swiss multinational that generates more than half its sales in the developing world.

4 Big Investing Trends You Can Bet On for the Next Several Years

If you don’t want to constantly worry about what percentage of your equity portfolio to keep in international shares, consider a global fund like Vanguard Total World ETF ( VT) . You’ll get a sampling of the entire world’s stock markets—including the U.S.—for just 0.14% in expenses a year. The fund currently has about 45% of its assets in international stocks, and seven percentage points of that

is in the emerging markets.

If you simply want international exposure, it’s hard to argue with Vanguard All-World ex-U.S. ETF ( VEU) , which charges just 0.13% a year. In addition to investing about 15% directly in emerging-markets stocks, this Vanguard fund has as its biggest holding Nestlé, the Swiss multinational that generates more than half its sales in the developing world.

4 Big Investing Trends You Can Bet On for the Next Several Years

The rise of portfolio isolationism and why you must resist

US investors shun foreign stocks. Why you shouldn't

- The bull market has been much more profitable for U.S. stocks than for international.

- U.S. investors are increasingly at risk of a home-based bias for recent performance.

- Long-term strategic and near-term fundamentals suggest now is not the time to shirk international stocks.

US investors shun foreign stocks. Why you shouldn't

Advertisement - Members don't see this ad

D

deleted50478

We will check this thread in 10 years and see how we did.

BMW’s i Vision Dynamics targets Tesla-topping range in a four-door coupe

When it is out for production I'll believe it.

You have to realize that Tesla has over 10 years head start (and a lot of $$$ invested) in infrastructure (charging stations) over any competitor.

Gas stations are not proprietary, for good reason. That Tesla charging station infrastructure is not the big deal it seems you think it is.When it is out for production I'll believe it.

You have to realize that Tesla has over 10 years head start (and a lot of $$$ invested) in infrastructure (charging stations) over any competitor.

If electric vehicles are going to ever become the norm, the charging stations can't be proprietary to the car's maker.

Imagine a gas station that could only pump gas into Fords, and a few miles off there was a station that could only pump gas into Hondas. Who would buy either? I'll tell you - an inconsequentially small group of people with special needs, or $ to indulge an impractical whim.

Do not disagree but in the case of a BMW charging at a Tesla station I'm sure it will monetized by the owner of the station, which will make Tesla even stronger.Gas stations are not proprietary, for good reason. That Tesla charging station infrastructure is not the big deal it seems you think it is.

If electric vehicles are going to ever become the norm, the charging stations can't be proprietary to the car's maker.

Imagine a gas station that could only pump gas into Fords, and a few miles off there was a station that could only pump gas into Hondas. Who would buy either? I'll tell you - an inconsequentially small group of people with special needs, or $ to indulge an impractical whim.

I doubt that too. Gas stations don't make much money on gas; they make money on the associated minimart. The attractive thing about electric cars is they're powered by electricity, which is cheaper than gas. There's no reason to think that margins selling electricity are going to be better than margins selling gas. Especially when 99% of electric car charging is going to be at home, not on long road trips ... there just ain't never going to be any money made selling electricity at the roadside.Do not disagree but in the case of a BMW charging at a Tesla station I'm sure it will monetized by the owner of the station, which will make Tesla even stronger.

Those charging stations are probably going to end up a source of loss for Tesla in the end, and they'll probably sell them off as soon as they can. The only reason they're building them at all is to help sell their cars.

The halo silicone valley companies not going anywhere are:

Amazon, google, Facebook and Apple

I wouldn't buy Snapchat even if it looks like how Facebook tanked after its ipo. Snapchat doesn't have the user base like Facebook.

I also think Visa and MasterCard are solid plays the next 3 years.

Amazon, google, Facebook and Apple

I wouldn't buy Snapchat even if it looks like how Facebook tanked after its ipo. Snapchat doesn't have the user base like Facebook.

I also think Visa and MasterCard are solid plays the next 3 years.

This is not a how to invest thread.

This is a place to recommend a stock that you think will do well.

We know some folks like Pacira, Cipotle, etc.

What other stocks do we like?

I'll start: Tesla

Why? Self driving trucks in the horizon.

I'm a contrarian investor. This requires patience and risk because it may take 2 years for the turn around. I generally allocate no more than 3% of my portfolio to individual stock picks and I typically buy only S and P 500 companies which are out of favor:

1. GE- risky. You get a dividend but management needs to turn the ship around.

2. QCOM- risky. Company is involved in a big lawsuit with Apple. But, if they win or settle the suit for 75% of the requested money the stock goes way up.

3. Macy's- The real estate value of Macys is likely worth more than the stock is trading at now.

4. Bank of America- Citigroup is the one the analysts all seem to love more but Buffet has faith in BAC

This is not a how to invest thread.

This is a place to recommend a stock that you think will do well.

We know some folks like Pacira, Cipotle, etc.

What other stocks do we like?

I'll start: Tesla

Why? Self driving trucks in the horizon.

You are arguing against yourself. If what you say is true, why would Tesla ever allow BMW charge there?I doubt that too. Gas stations don't make much money on gas; they make money on the associated minimart. The attractive thing about electric cars is they're powered by electricity, which is cheaper than gas. There's no reason to think that margins selling electricity are going to be better than margins selling gas. Especially when 99% of electric car charging is going to be at home, not on long road trips ... there just ain't never going to be any money made selling electricity at the roadside.

Those charging stations are probably going to end up a source of loss for Tesla in the end, and they'll probably sell them off as soon as they can. The only reason they're building them at all is to help sell their cars.

Make BMW put up their own money losing station at their own cost if they want to compete.

Either Tesla wins or BMW loses.

Advertisement - Members don't see this ad

This one?LAND - read the recent Barron's article on it.

Rich Farm Soil, Cheap REIT Stock

I don't subscribe, thus I can't read.

Isn't the dividend too low for a REIT? You pay full income taxes on REITS.

Neither Ford nor Honda "lose" or "win" when Exxon or 7-11 open or close a gas station.

What I'm arguing is that the existence of charging stations today, proprietary or not, has exactly zero relevance to which auto manufacturer will ultimately "lose" or "win" ... because 99% of electric vehicle charging happens at home. You seem to think that Tesla getting some kind of head start on this dead end retail electricity selling business gives them a leg up on BMW. I think that's a bizarrely silly thing to think.

Ultimately Tesla and BMW and other manufacturers will sell, or not sell, their cars on the strength or weakness of their cars.

At some point, Exxon and 7-11 will install charging stations with cables for different manufacturers, or cables for whatever standardized interface the car manufacturers agree on.

In any case. Whether or not Tesla's plan to open a bunch of charging stations will help them sell more cars ... this is a "recommend me a stock" thread ... the folly isn't in whichever one of is is wrong about this. It's in whichever one of us thinks he knows something the market doesn't and picks a stock based on that belief. Because even if you're right, that advantage or disadvantaged is already priced into the stock today.

The time to buy or dump Tesla's stock because of their charging station plan was the day before they announced their charging station plan.

What I'm arguing is that the existence of charging stations today, proprietary or not, has exactly zero relevance to which auto manufacturer will ultimately "lose" or "win" ... because 99% of electric vehicle charging happens at home. You seem to think that Tesla getting some kind of head start on this dead end retail electricity selling business gives them a leg up on BMW. I think that's a bizarrely silly thing to think.

Ultimately Tesla and BMW and other manufacturers will sell, or not sell, their cars on the strength or weakness of their cars.

At some point, Exxon and 7-11 will install charging stations with cables for different manufacturers, or cables for whatever standardized interface the car manufacturers agree on.

In any case. Whether or not Tesla's plan to open a bunch of charging stations will help them sell more cars ... this is a "recommend me a stock" thread ... the folly isn't in whichever one of is is wrong about this. It's in whichever one of us thinks he knows something the market doesn't and picks a stock based on that belief. Because even if you're right, that advantage or disadvantaged is already priced into the stock today.

The time to buy or dump Tesla's stock because of their charging station plan was the day before they announced their charging station plan.

Time will tell.Neither Ford nor Honda "lose" or "win" when Exxon or 7-11 open or close a gas station.

What I'm arguing is that the existence of charging stations today, proprietary or not, has exactly zero relevance to which auto manufacturer will ultimately "lose" or "win" ... because 99% of electric vehicle charging happens at home. You seem to think that Tesla getting some kind of head start on this dead end retail electricity selling business gives them a leg up on BMW. I think that's a bizarrely silly thing to think.

Ultimately Tesla and BMW and other manufacturers will sell, or not sell, their cars on the strength or weakness of their cars.

At some point, Exxon and 7-11 will install charging stations with cables for different manufacturers, or cables for whatever standardized interface the car manufacturers agree on.

In any case. Whether or not Tesla's plan to open a bunch of charging stations will help them sell more cars ... this is a "recommend me a stock" thread ... the folly isn't in whichever one of is is wrong about this. It's in whichever one of us thinks he knows something the market doesn't and picks a stock based on that belief. Because even if you're right, that advantage or disadvantaged is already priced into the stock today.

The time to buy or dump Tesla's stock because of their charging station plan was the day before they announced their charging station plan.

There is no doubt Tesla has a huge advantage today because of it's supercharging network. However as more non Tesla charging stations emerge that advantage can erode fairly quickly.

But as of today would you buy a car that you drive in a 100 mile radius of you home or one that can take you from coast to coast?

But as of today would you buy a car that you drive in a 100 mile radius of you home or one that can take you from coast to coast?

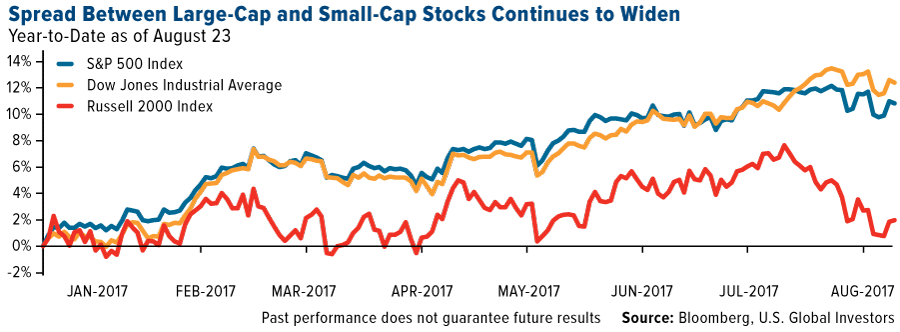

So in 9 months, small caps have underperformed. From 1980-2015 though, small caps averaged over 11% to 8% for large cap. This graph above totally cherry picked data by picking a time period that proves the point they're trying to make. Personally wouldn't read much into it.

EDIT: Also, in 2016, S&P500 was up 9.54%, Russell 2000 was up 20.7%. What is that suppossed to tell us then?

Last edited:

D

deleted50478

Samsung Unveils Electric Car Battery with a 435-Mile Range

The $85,000, Fully-Electric Porsche Mission E Will Arrive in 2019

Volvo, Betting on Electric, Moves to Phase Out Conventional Engines

If I could afford it I would buy a Tesla today. I hope they do well and I think they've had a positive impact of the future of transportation already, but there's a lot of competition on the horizon.

The $85,000, Fully-Electric Porsche Mission E Will Arrive in 2019

Volvo, Betting on Electric, Moves to Phase Out Conventional Engines

If I could afford it I would buy a Tesla today. I hope they do well and I think they've had a positive impact of the future of transportation already, but there's a lot of competition on the horizon.

Last edited by a moderator:

What about Equifax...? 🙄

Just means the market is lucrative. Otherwise not everyone and their grandmother will be jumping on it.Samsung Unveils Electric Car Battery with a 435-Mile Range

The $85,000, Fully-Electric Porsche Mission E Will Arrive in 2019

If I could afford it I would buy a Tesla today. I hope they do well and I think they've had a positive impact of the future of transportation already, but there's a lot of competition on the horizon.

Also let's hope the new Note 8 phone doesn't burn too many pockets.Samsung Unveils Electric Car Battery with a 435-Mile Range

The $85,000, Fully-Electric Porsche Mission E Will Arrive in 2019

If I could afford it I would buy a Tesla today. I hope they do well and I think they've had a positive impact of the future of transportation already, but there's a lot of competition on the horizon.

Fingers crossed.

What about Equifax...? 🙄

I bought some of EFX yesterday. It's oversold

Sent from my iPhone using SDN mobile

Advertisement - Members don't see this ad

AGN, BIIB, BX, DAL, GM, HALO, KR, LB, PCLN, TEVA, XOM

At least I can break even or make a few bucks when I buy stocks. In Vegas or buying lottery tickets I'm a loser almost every time. So, if you like to gamble a little then stock picking is the better way to put your money on the table.

"Oh, and if you still think the best route to financial success is by picking stocks, don’t show this article to your spouse."

That's why I limit stock selection to 3% of my portfolio. It's really hard to pick winners outside the growth tech sector.

Wouldn't touch AGN, HALO, LB, TEVA, or PCLN with a 10 foot pole.AGN, BIIB, BX, DAL, GM, HALO, KR, LB, PCLN, TEVA, XOM

Oil is not my thing. GM cars or airlines either.

That leaves BIIB, BX, KR.

Good tip.

D

deleted682700

SBI Holdings Feels Ripple can Become the Global Digital Banking Standard • r/Ripple

XRP. May be the first government approved crypto.

XRP. May be the first government approved crypto.

D

deleted682700

SBI Holdings Feels Ripple can Become the Global Digital Banking Standard •

Ripple has done extremely well. We used to have an ICU physician, Dr Lawrence Martin, whose advice was to take the money and run if you did make some money

Is bit coin a psyop

SBI Holdings Feels Ripple can Become the Global Digital Banking Standard • r/Ripple

XRP. May be the first government approved crypto.

Freaking Genius Call with 500% returns over 3 months.

XRP

The digital currency ended 2016 at less than 1 cent and topped $1 only last week, before leaping above $2 Friday afternoon. Ripple is up more than 34,700 percent this year.

The digital currency ended 2016 at less than 1 cent and topped $1 only last week, before leaping above $2 Friday afternoon. Ripple is up more than 34,700 percent this year.

I'm still tilting towards International Small Cap and Emerging Markets for 2018. If the global recovery holds up I expect 20+% returns in these sectors.

Domestically, Energy and Financials look like good bets so I'm overweighting Energy ETFs and buying some energy stocks. This sector has been CRUSHED the past 5 years with most ETFs still negative over 5 years.

I think TECH will still work in 2018 but likely less stellar returns vs 2017 as most are fully valued. I like Facebook, MSFT, Google and Amazon but not sure how much juice they have left in them at these valuations.

CNBC commentators like Constellation Brands and Agriculture stocks like Potash or Mosaic.

MY bet is for a 7-10% increase in the S and P 500 over the next 12 months with more volatility. I'm expecting 20% returns for some foreign equities and emerging markets.

As for Crypto, I have no idea as I don't get why this stuff has any value at all. But, many like a trip to Vegas and buying Crypto is almost as good.

Domestically, Energy and Financials look like good bets so I'm overweighting Energy ETFs and buying some energy stocks. This sector has been CRUSHED the past 5 years with most ETFs still negative over 5 years.

I think TECH will still work in 2018 but likely less stellar returns vs 2017 as most are fully valued. I like Facebook, MSFT, Google and Amazon but not sure how much juice they have left in them at these valuations.

CNBC commentators like Constellation Brands and Agriculture stocks like Potash or Mosaic.

MY bet is for a 7-10% increase in the S and P 500 over the next 12 months with more volatility. I'm expecting 20% returns for some foreign equities and emerging markets.

As for Crypto, I have no idea as I don't get why this stuff has any value at all. But, many like a trip to Vegas and buying Crypto is almost as good.

Last edited:

The Domestic stock market is fully valued but the TAX CUT will add some juice to the valuations; But, will the market run out of of juice by the summer? I'm expecting some big pullbacks in 2018 but an overall positive year. 2018 may be the last year of this bull cycle:

- The Morningstar Global Markets Index has returned more than 23% over the past year.

- The market-cap-weighted price/fair value ratio for our equity analysts' coverage universe is 1.06.

- Communication services is the most undervalued sector, with a price/fair value ratio of 0.93. Basic materials is the most overvalued sector, with a price/fair value ratio of 1.39.

Advertisement - Members don't see this ad

Similar threads

- Replies

- 0

- Views

- 736