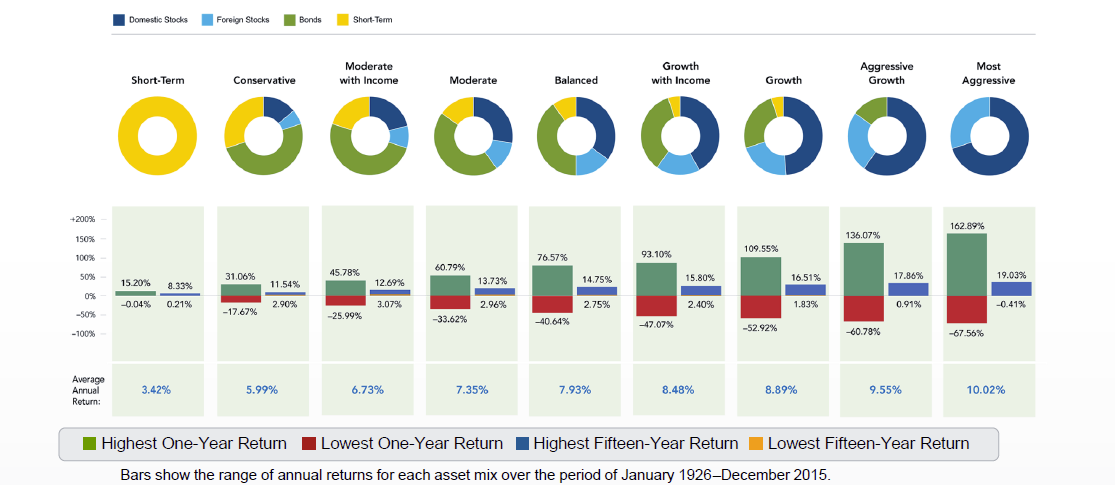

The portfolio below is a good one. You could include REITS (domestic and international) by reducing the Bond Fund exposure to 10%. Maybe skip the long term bond fund in favor of an intermediate bond fund (5%) and a short term bond fund (5%) but if you think the 10 year yield on US debt isn't going any higher then the long term bond may be a better investment for you.

Vanguard S&P 500 ETF (NYSEARCA:VOO) or Vanguard Admiral Shares (MUTF:VFIAX) - This Vanguard 500 Index Fund buys the 500 stocks selected by S&P to represent the U.S. large cap stock universe. It has the advantage of being an index that is recognized and purchased around the world. A limited number of stocks with growing global demand and an incredibly low 0.05% expense ratio make this Vanguard S&P 500 index fund a good core holding for your portfolio.

Vanguard Extended Markets ETF (NYSEARCA:VXF) or Vanguard Admiral Shares (MUTF:VEXAX) - This fund contains all of the U.S. common stocks regularly traded on the New York Stock Exchange and the Nasdaq over-the-counter market, except those stocks included in the S&P 500 Index. This fund fills in the blanks that are missing from the S&P 500 Index. It holds a total of 3,078 US stocks, mostly mid and small caps, which gives you fantastic coverage of the U.S. stock market.

Vanguard Total International Stock ETF (NASDAQ:VXUS) or Vanguard Admiral Shares (MUTF:VTIAX) - This fund tracks the market-cap weighted FTSE Global All Cap ex US Index, which covers 99% of the world's global market capitalization outside the US. The ETF holds 5,512 stocks from 46 developed and emerging markets.

Vanguard FTSE Emerging Markets ETF (NYSEARCA:VWO) or Vanguard Admiral Shares (MUTF:VEMAX) - This fund offers investors a low-cost way to gain equity exposure to emerging markets. The fund invests in stocks of companies located in emerging markets around the world, such as Brazil, Russia, India, Taiwan, and China. The Vanguard Total International Stock fund listed above already includes these same Emerging Markets stocks but because it is market-cap weighted they do not have nearly as much influence as the larger companies in the fund. Due to the high volatility, I only add this Emerging Markets fund to my higher risk portfolios.

Vanguard Long Term Bond ETF (NYSEARCA:BLV) or Vanguard Investor Shares (MUTF:VBLTX) - This Vanguard bond fund tracks the Barclays U.S. Long Government/Credit Float Adjusted Index. This Index includes all publicly issued medium and larger issues of U.S. government, investment-grade corporate, and investment-grade international dollar denominated bonds that have maturities of greater than 10 years. This ETF uses a sampling method to replicate this index and currently holds 1,658 bonds.

Incredible diversification - Just five Vanguard investments and you will own 9,090 stocks and 1,658 bonds. This is a total of 10,748 holdings that you can buy for the cost of five Vanguard ETFs or Vanguard Index Funds, which are free to purchase if you use a Vanguard Brokerage account.

Vanguard ETF Portfolio For The Growth Investor | Seeking Alpha